Introduction:

Management Business Reviews (MBRs) are a crucial aspect of any organization’s decision-making process. These periodic meetings bring together key stakeholders to assess the company’s performance, review financial results, discuss strategies, and make informed decisions. In this article, we will delve into the significance of MBRs and provide valuable insights on how to successfully present financial results during these critical meetings.

Understanding Management Business Reviews (MBRs):

MBRs, also known as Business Performance Reviews (BPRs) or Executive Business Reviews (EBRs), are structured meetings that typically occur monthly, quarterly, or annually. Almost every business organization conducts these types of meetings in some form. Their primary objectives include:

- Performance Assessment: Evaluate the company’s overall performance against predefined goals and key performance indicators (KPIs).

- Strategy Alignment: Ensure that current activities align with the company’s strategic objectives.

- Issue Identification: Identify challenges, roadblocks, and opportunities for improvement.

- Decision-Making: Make informed decisions based on the data and insights presented.

Key Components of a Successful MBR:

To conduct a productive MBR, consider the following components:

1. Clear Agenda:

Define a well-structured agenda outlining the topics to be discussed. Include time slots for each item to maintain focus and manage time effectively. It is a good idea to develop a template (e.g. using PowerPoint), that is shared with business and financial leaders, to be followed. This helps ensure consistency and alignment. Specially, if there are multiple business units having separate business reviews.

2. Financial Reports:

Financial results are a MUST have for all management business reviews. Present comprehensive financial reports, including income statements, balance sheets, and cash flow statements. Highlight key financial metrics and variances from previous periods or targets. Whether you are a Finance professional or business leader, it is essential that you know and understand your numbers. This comes with time and experience, but there is a base level of technical know-how that is required to explain financial reports. Here is a course we have developed to analyze and explain income statement and EBITDA performance in management meetings. Click on https://ebitda.thinkific.com/courses/learn to access the course at a special (heavy) discount for the readers of this article.

3. Operational Metrics:

Incorporate operational metrics that provide a holistic view of the business. These may include customer satisfaction scores, employee productivity, or market share data. Again, it is key to understand the calculations, how the KPIs are calculated in your organization, any issues with data accuracy and how to interpret those KPIs.

4. SWOT Analysis:

Conduct a SWOT (Strengths, Weaknesses, Opportunities, Threats) analysis to assess the internal and external factors affecting the company’s performance. You should always have a SWOT analysis available for discussion. It is a good idea to keep it as a LIVE document and update based on the most recent circumstances (both external and internal).

5. Strategy Review:

Review the current strategic initiatives and their progress. Discuss any necessary adjustments to align with changing market conditions or organizational goals. Strategies can and should be adjusted based on market conditions. Regularly reviewing strategies helps the business stay ahead of the competitors and market fluctuations.

6. Action Items:

Document action items arising from the meeting, assign responsibilities, and set deadlines for implementation. Ensure follow-up in subsequent MBRs.

Successfully Presenting Financial Results in an MBR:

Now, let’s focus on how to effectively present financial results during an MBR:

1. Know Your Audience:

Understand the background and knowledge level of the participants. Tailor your presentation to address their concerns and interests. There usually are some current issues or hot topics related to each business unit. Make sure those are addressed. Be thoughtful in presenting the analysis or update on the issue. How can you use visualizations and charts to convey the message more concisely.

2. Use Visual Aids:

This point is obvious. Utilize charts, graphs, and tables to illustrate financial data. Visual aids make complex information more digestible and memorable. The better you are at doing this, the more knowledgeable and competent you will be perceived. This could be the differentiating factor between your presentations and others in the organization.

3. Focus on Key Metrics:

Highlight key financial metrics that align with the company’s goals and strategies. These may include revenue growth, profitability, cash flow, and return on investment. Most leaders already like to see certain metrics and KPIs and request for them. Make sure those are included, but think outside the box. What additional information that is relevant and insightful can you add. Again keep it simple and intuitive. Less is more.

4. Explain Variances:

If there are significant variances from previous periods or targets, provide explanations. Was the variance due to external factors, changes in market conditions, or internal decisions? This can be a tough area for many finance and non-finance leaders. We have developed a thorough course on explaining income statement variances vs budget and prior year. This course helps you explain variances in amounts and percentages e.g. change in gross profit % or EBITDA %. We highly recommend you take this course by clicking on https://ebitda.thinkific.com/courses/learn

5. Tell a Story:

Narrate the financial results as a story. Always keep this in the back of your mind. Can you convert the numbers, tables, charts and graphs into a story? Explain how the numbers translate into real-world impact, both positive and negative.

6. Provide Context:

Offer context for the financial results. Discuss industry trends, competitive positioning, and market dynamics that may have influenced the numbers.

7. Discuss Risk Mitigation:

Address any financial risks and mitigation strategies. This demonstrates foresight and proactive planning.

8. Offer Solutions:

If there are financial challenges or underperformance, propose solutions. Engage the participants in a constructive discussion about potential actions.

9. Q&A and Discussion:

Encourage questions and discussions throughout the presentation. Be prepared to provide detailed answers and engage in productive dialogues.

10. Summarize Key Takeaways:

Conclude the financial presentation by summarizing the key takeaways, action items, and decisions made during the meeting.

Conclusion:

Management Business Reviews are essential for organizations to assess their performance, align strategies, and make informed decisions. Effectively presenting financial results during an MBR requires thorough preparation, clear communication, and a focus on key metrics and actionable insights. By following these guidelines, financial professionals can contribute to more productive and insightful MBRs, ultimately driving the success of the organization. Remember that MBRs are not just about numbers; they are a platform for collaboration, problem-solving, and strategic planning.

If you would like to take the first step towards really understanding income statement performance and present variance explanations during MBRs, check this video out. It should help you significantly.

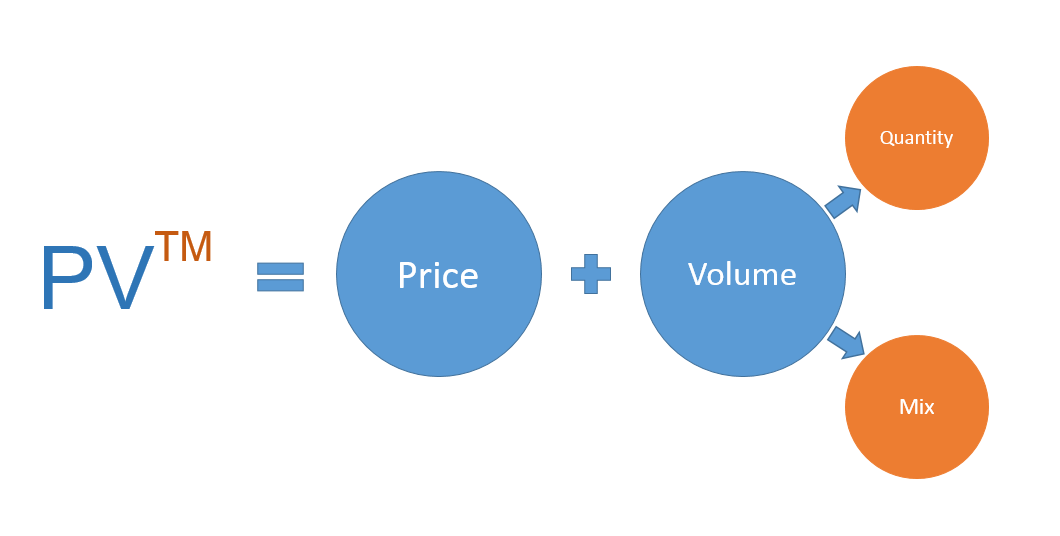

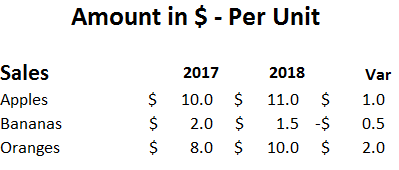

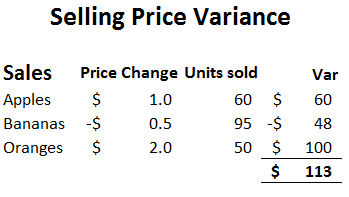

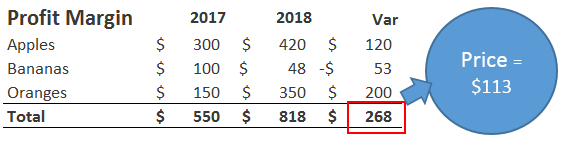

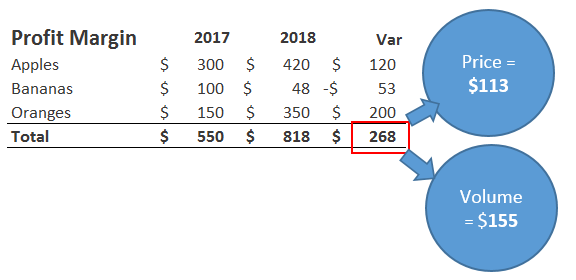

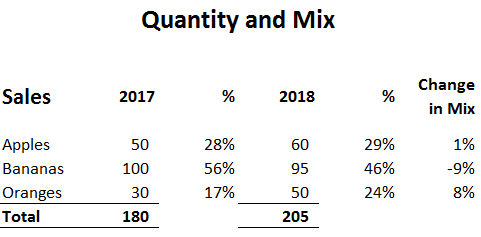

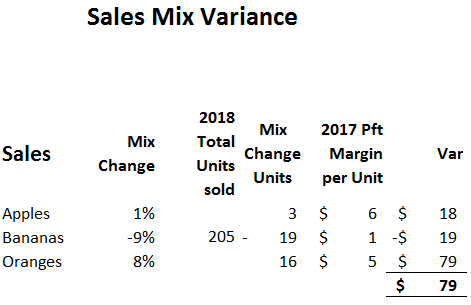

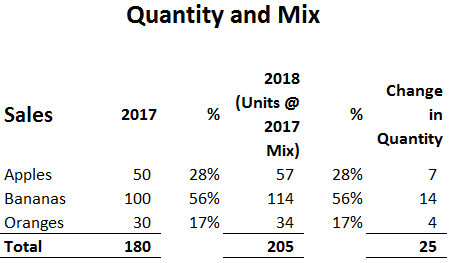

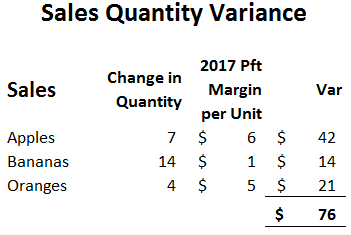

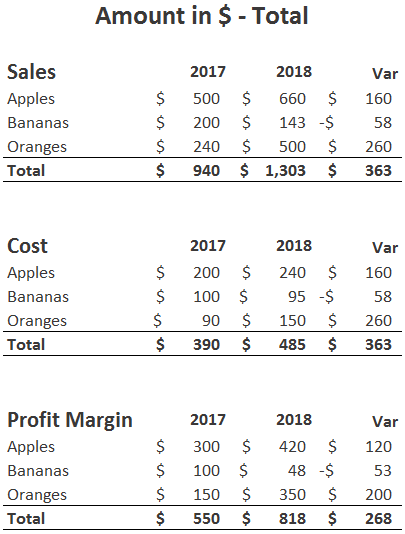

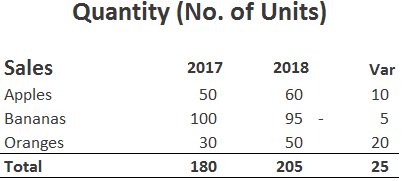

Types of Sales Variances

Types of Sales Variances